Business Advisory

Financial Planning for Medical Residents

Medical residency is a major milestone, but it also comes with unique financial challenges. Between student debt, limited income, and

Medical residency is a major milestone, but it also comes with unique financial challenges. Between student debt, limited income, and

Guaranteed Investment Certificates (GICs) are a popular choice for Canadians looking for stable, low-risk returns. But when tax season arrives,

If you live in Canada, April 30 is the deadline to file your personal income tax return and pay any

Graduating from nursing or medical school is an exciting milestone, but for many new healthcare professionals, tax season can quickly

Alberta’s UCP government has introduced Bill 11: the Health Statutes Amendment Act, 2025 (No. 2)—proposed legislation that would allow surgeons

Tax season can feel overwhelming for busy healthcare professionals, especially when patient care always comes first. For physicians and nurse

For clinic owners, investing in medical equipment is one of the most significant financial decisions you can make. Whether you’re

Graduating with student debt is a reality for many Canadians, and the idea of reducing or eliminating that debt can

At MMT Chartered Professional Accountants, we specialize in supporting medical professionals like physicians, nurse practitioners and those setting up their

Why Early Preparation Matters At MMT Chartered Professional Accountants, we help individuals, incorporated professionals, and business owners stay ahead of

Tips for Staying on Track The holiday season is a time for joy, family, and tradition. But it can also

The Short- and Long-Term Benefits of Topping Up As the calendar year winds down, many Canadians start thinking about their

As 2025 comes to a close, many clinics and small businesses across Canada are preparing for tax season. While filing

Year’s end is just around the corner, and it is becoming time to ensure your clinic’s tax planning is both

Integrated Tax, Wealth, and Assurance Strategies Work Best When They’re Aligned You wouldn’t expect your doctor, physiotherapist, and pharmacist to

New Capital Gains Rule Could Make Incorporation More Attractive in 2025 If you’re launching a medical practice in Calgary or

Moving to Vancouver as a newcomer to Canada brings exciting opportunities—but also a new set of responsibilities when it comes

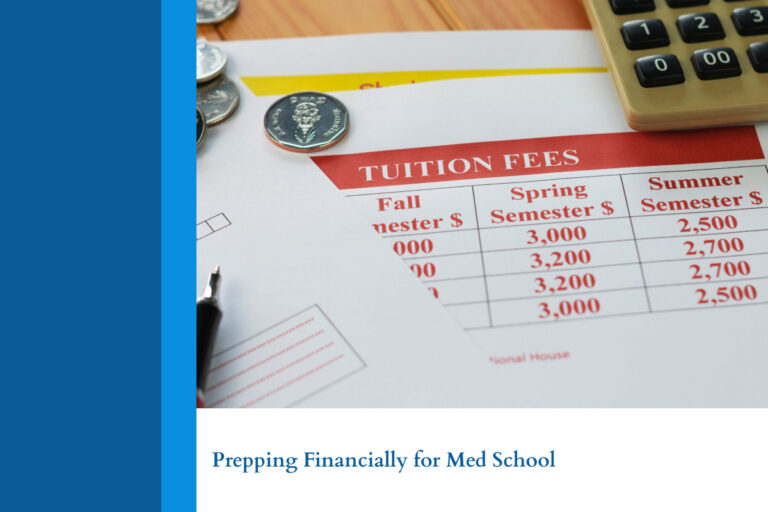

Entering medical school is an exciting milestone, but it also marks the beginning of a major financial commitment. With tuition,

Running a medical practice in Canada involves more than just patient care—it also includes staying on top of tax responsibilities,

What You Need to Know About Taxes This Summer As summer approaches and Canadians gear up for travel, many homeowners

Retirement planning is a complex but critical part of a physician’s financial journey. With years spent in education and training,

What Business Owners Need to Know About Payroll & Taxes Seasonal hiring can be a smart move for businesses that

Opening an investment account is a smart step toward building long-term wealth, whether saving for retirement, your children’s education, or

Buying a clinic is a significant milestone in a physician’s career. Whether you’re an established practitioner or transitioning from an

Tax season is here, and we know you have questions! Whether you’re a long-time MMT CPA client or just looking